The costs of climate action have come down dramatically. Recently, the UK Energy Transition Committee estimated the cost for realizing a net-zero economy by 2050 at 0,5% of global GDP in a high cost scenario. This is substantially less than the estimate put forward in the 2006 Stern review, i.e. a cost of 1% of GDP to achieve net-zero by 2075.

Much of this difference can attributed to cost reductions in wind and solar energy, largely driven by technology developments, economies of scale, cost-effective supply chains and favourable incentivizing frameworks. Over the past decade costs for offshore wind power costs dropped 29% and they may fall further to below 0,04 €/kWh by 2030. Solar PV declined by as much as 82%. For solar PV very competitive prices are possible already now, even in new markets. In the Middle East, Ethiopia, Mexico and Peru auction prices have reached record lows. Last year, a bid price of 0,015 €/kWh was registered in Portugal, while average levelized costs for next year are estimated around 0,032 €/kWh.

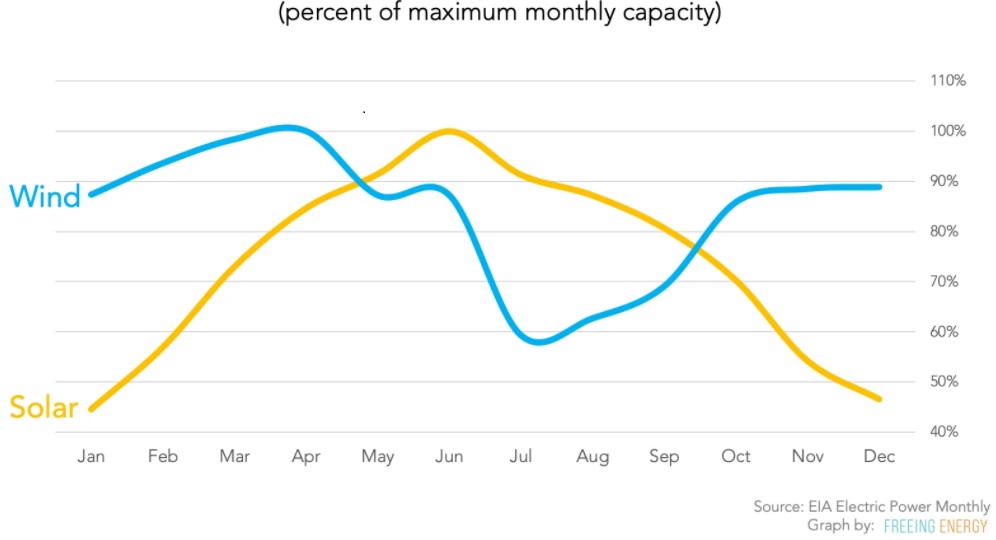

Considering their abundance and undefeated cost reductions it may come as no surprise that electricity from renewable sources is the core of the ongoing energy transition. After the eras of coal and natural gas, we now enter the age of green electricity. Other energy carriers may have a role too, but supplies are more expensive and restricted. A big plus is that green electricity can be transported speedily across the continent. Throughout the EU investments in high voltage power lines have increased considerably, due to market integration and the need for a secure supply. Investments in gas networks have been considerably lower, since they are less developed in many countries and because gas consumption fell by 10%. Moreover, while wind and solar are intermittent sources, their combined application goes a long way in mitigating the seasonal variability of either resource, with solar-PV peaking in summer and wind yields typically higher in winter.

Figure 1 Illustration of capacity utilization rates for wind and solar. Source: EIA, graph by FreeingEnergy.com

Back-up systems are an important solution to any remaining intermittency, and developments are promising. The cost of lithium-ion batteries has decreased sharply, driven by a surge in the uptake of electric vehicles. By 2030, battery sizes will be around 70-80 kWh, and they may well have a second life in stationary applications in homes with limited investment costs. A 80 kWh battery could provide a typical 200 W for a normal home during 400 hours.

Backup facilities are also important at a larger scale. Stationary fuel cells can provide emergency capacity for industrial and commercial purposes whenever wind and sun are absent. A fuel cell is basically the reverse of an electrolyser as it converts hydrogen and oxygen into water while producing electricity. Fuel cells are efficient, clean, almost silent, and reliable. Bosch had good reasons to announce this month that it will start building 200 MW of stationary fuel cell capacity each year.

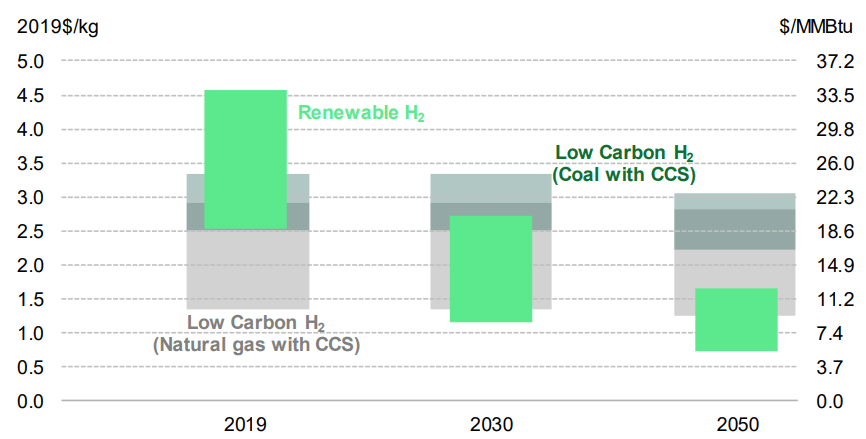

Until recently, the limited availability of hydrogen hampered the uptake of stationary fuel cells, but this is changing. Hydrogen is a versatile product that may be applied as a feedstock or energy carrier in industry and transport. It can be produced free of carbon through electrolysis, a process in which green electricity is used to decompose water into hydrogen and oxygen, basically the reverse of a fuel cell. Such green hydrogen must and will become cheaper, and not only because the cost of electrolysers may fall by 70% in the coming decade. More important even are the cost reductions for green electricity, as mentioned. As a result levelized costs of green hydrogen production may drop from the 2,5-4.5 $/kg range today to under 1,5 $/kg by 2050. Any transport costs would be comparable to the cost of shipping oil today. Thus, green hydrogen production with solar-PV at low geographical latitudes could compete successfully with other production routes.

Figure 2 Levelized cost of hydrogen production (global). Source: Bloomberg NEF, 2019.

All of this matters in particular since Shell is currently on trial in The Netherlands over its failure to cut carbon emissions, brought to court by Milieudefensie, an environmental ngo. The company may well be compelled to present a convincing strategy for advancing a net-zero future by 2050.

Current plans for a large blue hydrogen project in The Netherlands, in which Shell partners, are valued up to 12 €billion. Apart from the initial investment this includes operational costs for hydrogen production, and for CO2 transport and storage over the project lifetime. Costs of CO2 avoided will be 86 to 190 €/t, depending on the project scope. This is far from cheap, and would imply a fossil investment that could impossibly be depreciated by 2050.

Instead, it would be wiser to elaborate an investment plan with offshore wind centre stage, combined with the production of green hydrogen, once costs for offshore wind are sufficiently low. On a very short term, Shell could already start producing green hydrogen from solar-PV at lower latitudes, where Shell has had assets for many years. This hydrogen could be used in industry and transport, as well as in backup power facilities. Finally, Shell could step up efforts to make synthetic fuels through Power-to-Liquids technology a success, in close collaboration with the aviation sector.

That would allow the Age of Green Power to truly take off.